Kvanefjeld Rare Earths

Kvanefjeld Rare Earths

Kvanefjeld is a globally significant rare earth project with the potential to become a major Western supplier of critical rare earth elements.

Located in southern Greenland with year-round direct shipping access, Kvanefjeld hosts a Mineral Resource in accordance with the JORC Code of 1 billion tonnes grading 1.1% Rare Earth Oxides (REO) containing 1.14Mt of contained REO across three different zones – Kvanefjeld, Sørensen and Zone 3. The resource table can be viewed here: Mineral Resource Table

Key Project Advantages

Kvanefjeld has a number of unique attributes that make it attractive as a development opportunity:

Infrastructure

Located <10km from an ice-free deep-water fjord

Year-round direct shipping access (no ice-roads required)

Access to hydropower and nearby Narsarsuaq airport

Favourable Process & Metallurgy

Non-refractory mineralogy relative to many REE deposits

Conventional flotation and leaching routes demonstrated

Multiple pilot scale processing campaigns completed

Significantly De-Risked Through Extensive Studies

More than a decade of sustained technical work

Pre-Feasibility and Feasibility Studies completed historically

Bulk sampling and metallurgical testwork undertaken

These attributes position Kvanefjeld as a potential long-life supplier of rare earths to Western markets.

Legal Proceedings

The development of Kvanefjeld remains halted following the passing of Act No. 20 of 2021 (the “Uranium Act”) by the Greenlandic legislature, which prohibits the exploration and production of uranium mineralisation.

In response, ETM has initiated arbitration and litigation proceedings against the Governments of Greenland and Denmark. Following recent rulings, ETM is now focused on litigation to be heard in the High Court of Greenland, while preserving its rights in the related arbitration and Danish proceedings, where it has filed a Statement of Claim with an Arbitral Tribunal seated in Copenhagen.

The full Statement of Claim will be provided on request to enquires address to arbitration@etransmin.com.

The Summary of Dispute and Statement of Claim are available here:

While these legal processes may extend over several years, the Board remains confident in the merits of ETM’s position, while at the same time continuing to pursue a constructive and amicable resolution through transparent engagement with all key stakeholders.

“ We remain resolute in our intention to develop Kvanefjeld responsibly and in accordance with international best practice, cognisant of the life-changing opportunities and economic returns the project can generate.”

Environmental & Social Impact Assessment

The Environmental Impact Assessment (EIA) provides an assessment of the potential environmental impacts of the Kvanefjeld rare earth (REE) project and describes the environmental management practices that will be in place during the Project’s construction, operations, closure and post-closure phases.

The Project includes integrated mine, processing plant, and port facilities. The EIA was released for public consultation in 2020, following a lengthy process that commenced following the preparation of an initial feasibility study in 2010, including public consultation on the Terms of Reference of the EIA, technical studies, and feedback from regulators.

Understanding Naturally Occurring Radioactive Material

ETM had met all legal and licence requirements and was finalising responses to the Environmental and Social Impact Assessments when the “Uranium Act” was introduced in Greenland. The Government now claims the Uranium Act blocks the grant of the Kvanefjeld Exploitation Licence. ETM is pursuing both arbitration and litigation to enforce its legal right to the licence (see Arbitration Proceedings above).

The following information guides provide further information on uranium at Kvanefjeld and an overview of naturally occurring radioactive material:

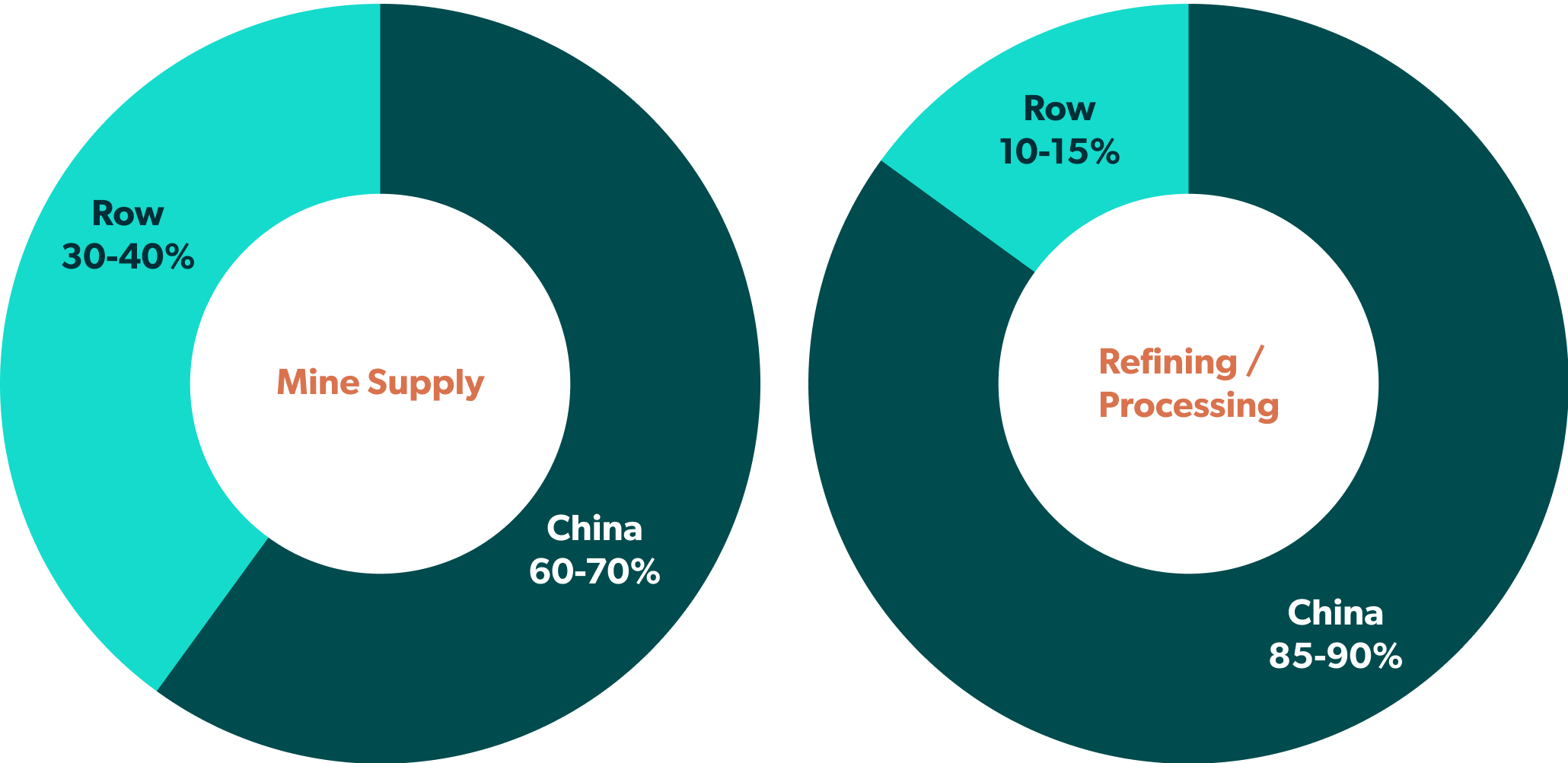

Market Opportunity

The Kvanefjeld Project is ideally positioned to help diversify global rare earths supply chains.

Rare Earths Production Share1

- Significant opportunity to diversify the global supply chain for rare earths

- Supply concentration now viewed as strategic risk

- Large-scale assets increasingly strategic

- Magnet REE demand supported by energy transition and defence applications

1. Source: U.S. Geological Survey, Mineral Commodity Summaries 2025; International Energy Agency, Global Critical Minerals Outlook 2025 Notes: Figures are indicative and represent approximate ranges based on publicly available government and intergovernmental data. Percentages may vary by reporting year, methodology, and definitions of production and processing stages. No assurance is given as to future supply, demand, market share, or policy outcomes.